4. Examples

The following examples are available in a checkout of the repository

in the examples/ directory.

4.1. MCMC

'''This example illustrates how to run a Markov Chain using pypmc'''

import numpy as np

import pypmc

# define a proposal

prop_dof = 1.

prop_sigma = np.array([[0.1 , 0. ]

,[0. , 0.02]])

prop = pypmc.density.student_t.LocalStudentT(prop_sigma, prop_dof)

# define the target; i.e., the function you want to sample from.

# In this case, it is a Gaussian with mean "target_mean" and

# covariance "target_sigma".

#

# Note that the target function "log_target" returns the log of the

# unnormalized gaussian density.

target_sigma = np.array([[0.01 , 0.003 ]

,[0.003, 0.0025]])

inv_target_sigma = np.linalg.inv(target_sigma)

target_mean = np.array([4.3, 1.1])

def unnormalized_log_pdf_gauss(x, mu, inv_sigma):

diff = x - mu

return -0.5 * diff.dot(inv_sigma).dot(diff)

log_target = lambda x: unnormalized_log_pdf_gauss(x, target_mean, inv_target_sigma)

# choose a bad initialization

start = np.array([-2., 10.])

# define the markov chain object

mc = pypmc.sampler.markov_chain.AdaptiveMarkovChain(log_target, prop, start)

# run burn-in

mc.run(10**4)

# delete burn-in from samples

mc.clear()

# run 100,000 steps adapting the proposal every 500 steps

# hereby save the accept count which is returned by mc.run

accept_count = 0

for i in range(200):

accept_count += mc.run(500)

mc.adapt()

# extract a reference to the history of all visited points

values = mc.samples[:]

accept_rate = float(accept_count) / len(values)

print("The chain accepted %4.2f%% of the proposed points" % (accept_rate * 100) )

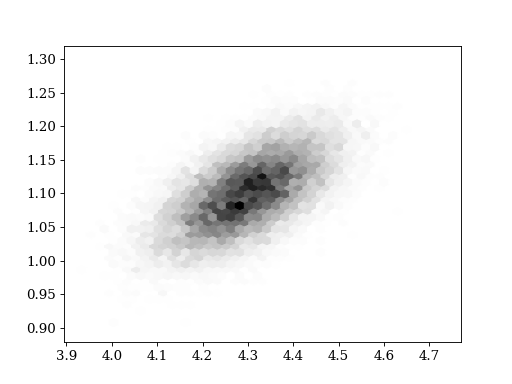

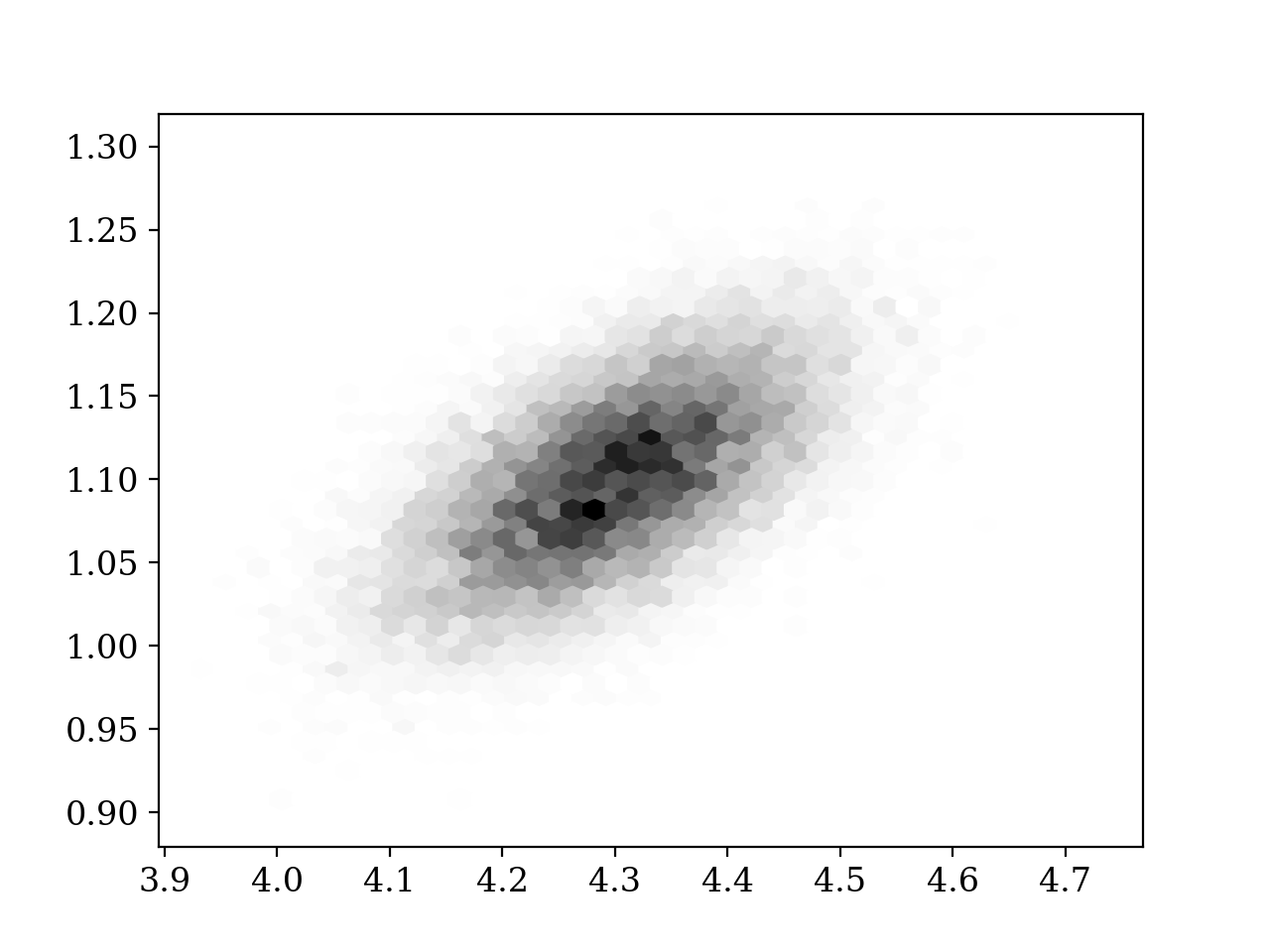

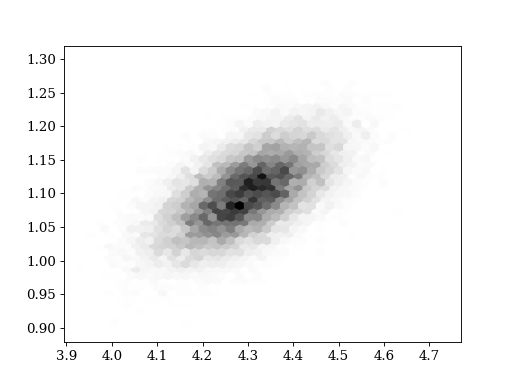

# plot the result

try:

import matplotlib.pyplot as plt

except ImportError:

print('For plotting "matplotlib" needs to be installed')

exit(1)

plt.hexbin(values[:,0], values[:,1], gridsize = 40, cmap='gray_r')

plt.show()

(Source code, png, hires.png, pdf)

{kind=link}

{kind=link}

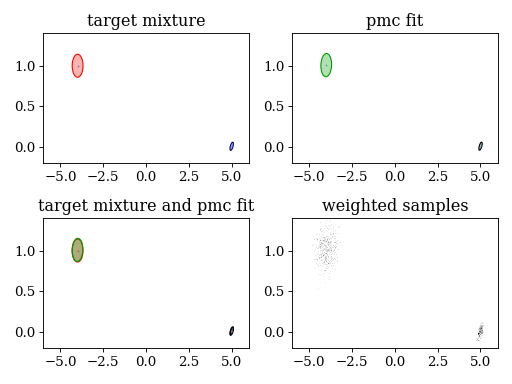

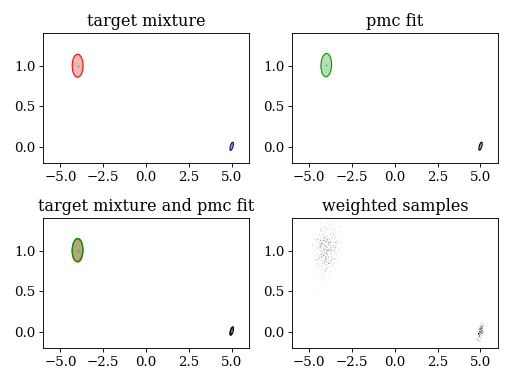

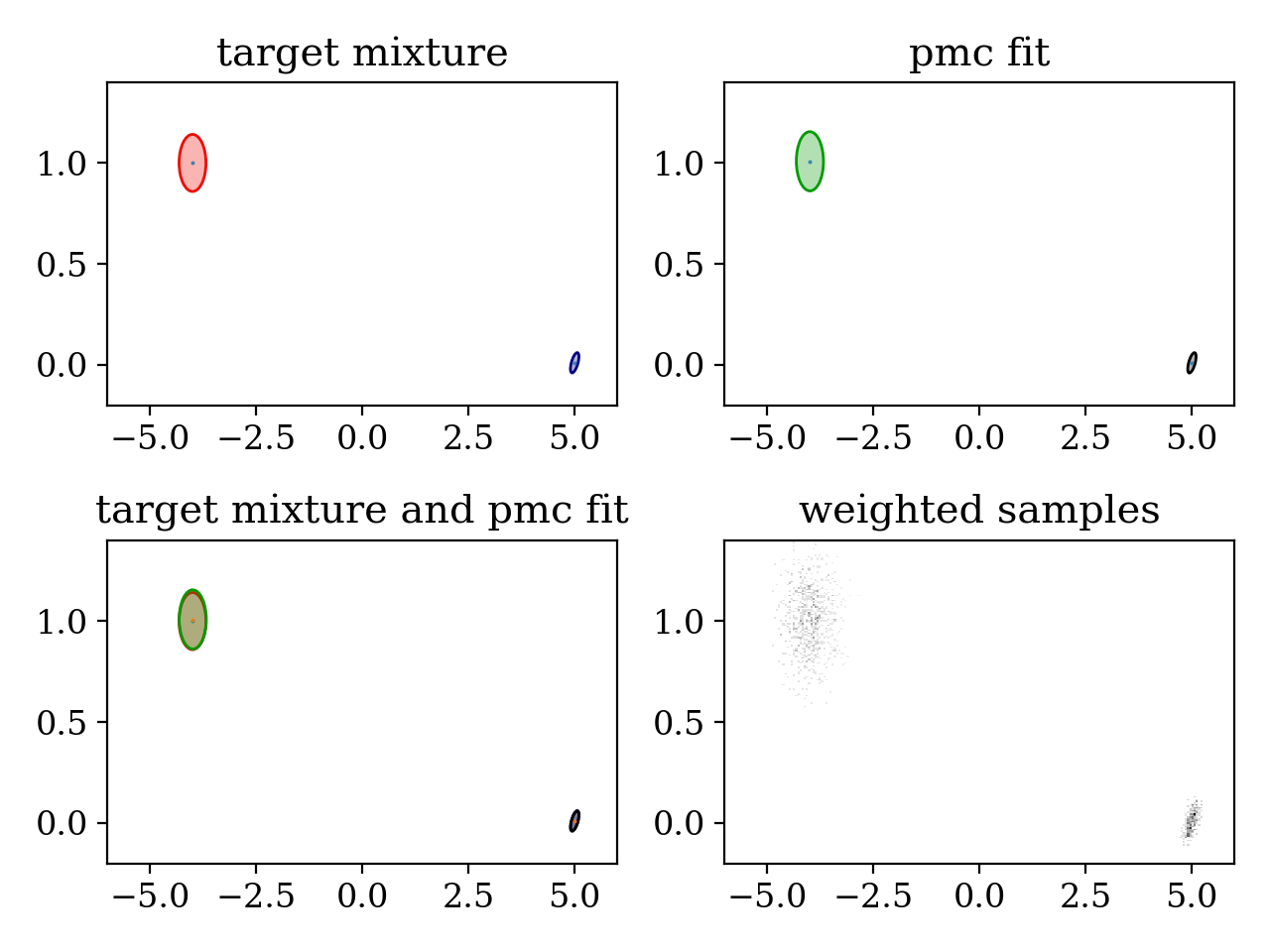

4.2. PMC

4.2.1. Serial

'''This example shows how to use importance sampling and how to

adapt the proposal density using the pmc algorithm.

'''

import numpy as np

import pypmc

# define the target; i.e., the function you want to sample from.

# In this case, it is a bimodal Gaussian

#

# Note that the target function "log_target" returns the log of the

# target function.

component_weights = np.array([0.3, 0.7])

mean0 = np.array ([ 5.0 , 0.01 ])

covariance0 = np.array([[ 0.01 , 0.003 ],

[ 0.003, 0.0025]])

inv_covariance0 = np.linalg.inv(covariance0)

mean1 = np.array ([-4.0 , 1.0 ])

covariance1 = np.array([[ 0.1 , 0. ],

[ 0. , 0.02 ]])

inv_covariance1 = np.linalg.inv(covariance1)

component_means = [mean0, mean1]

component_covariances = [covariance0, covariance1]

target_mixture = pypmc.density.mixture.create_gaussian_mixture(component_means, component_covariances, component_weights)

log_target = target_mixture.evaluate

# define the initial proposal density

# In this case a three-modal gaussian used

# the initial covariances are set to the unit-matrix

# the initial component weights are set equal

initial_prop_means = []

initial_prop_means.append( np.array([ 4.0, 0.0]) )

initial_prop_means.append( np.array([-5.0, 0.0]) )

initial_prop_means.append( np.array([ 0.0, 0.0]) )

initial_prop_covariance = np.eye(2)

initial_prop_components = []

for i in range(3):

initial_prop_components.append(pypmc.density.gauss.Gauss(initial_prop_means[i], initial_prop_covariance))

initial_proposal = pypmc.density.mixture.MixtureDensity(initial_prop_components)

# define an ImportanceSampler object

sampler = pypmc.sampler.importance_sampling.ImportanceSampler(log_target, initial_proposal)

# draw 10,000 samples adapting the proposal every 1,000 samples

# hereby save the generating proposal component for each sample which is

# returned by sampler.run

# Note: With too few samples components may die out, and one mode might be lost.

generating_components = []

for i in range(10):

print("\rstep", i, "...\n\t", end='')

# draw 1,000 samples and save the generating component

generating_components.append(sampler.run(10**3, trace_sort=True))

# get a reference to the weights and samples that have just been generated

samples = sampler.samples[-1]

weights = sampler.weights[-1][:,0]

# update the proposal using the pmc algorithm in the non Rao-Blackwellized form

pypmc.mix_adapt.pmc.gaussian_pmc(samples, sampler.proposal, weights, generating_components[-1],

mincount=20, rb=True, copy=False)

print("\rsampling finished")

print( '-----------------')

print('\n')

# print information about the adapted proposal

print('initial component weights:', initial_proposal.weights)

print('final component weights:', sampler.proposal.weights)

print('target component weights:', component_weights)

print()

for k, m in enumerate([mean0, mean1, None]):

print('initial mean of component %i:' %k, initial_proposal.components[k].mu)

print('final mean of component %i:' %k, sampler.proposal.components[k].mu)

print('target mean of component %i:' %k, m)

print()

print()

for k, c in enumerate([covariance0, covariance1, None]):

print('initial covariance of component %i:\n' %k, initial_proposal.components[k].sigma, sep='')

print()

print('final covariance of component %i:\n' %k, sampler.proposal.components[k].sigma, sep='')

print()

print('target covariance of component %i:\n' %k, c, sep='')

print('\n')

# plot results

try:

import matplotlib.pyplot as plt

except ImportError:

print('For plotting "matplotlib" needs to be installed')

exit(1)

def set_axlimits():

plt.xlim(-6.0, +6.000)

plt.ylim(-0.2, +1.401)

plt.subplot(221)

plt.title('target mixture')

pypmc.tools.plot_mixture(target_mixture, cmap='jet')

set_axlimits()

plt.subplot(222)

plt.title('pmc fit')

pypmc.tools.plot_mixture(sampler.proposal, cmap='nipy_spectral', cutoff=0.01)

set_axlimits()

plt.subplot(223)

plt.title('target mixture and pmc fit')

pypmc.tools.plot_mixture(target_mixture, cmap='jet')

pypmc.tools.plot_mixture(sampler.proposal, cmap='nipy_spectral', cutoff=0.01)

set_axlimits()

plt.subplot(224)

plt.title('weighted samples')

plt.hist2d(sampler.samples[-1][:,0], sampler.samples[-1][:,1], weights=sampler.weights[-1][:,0], cmap='gray_r', bins=200)

set_axlimits()

plt.tight_layout()

plt.show()

(Source code, png, hires.png, pdf)

{kind=link}

{kind=link}

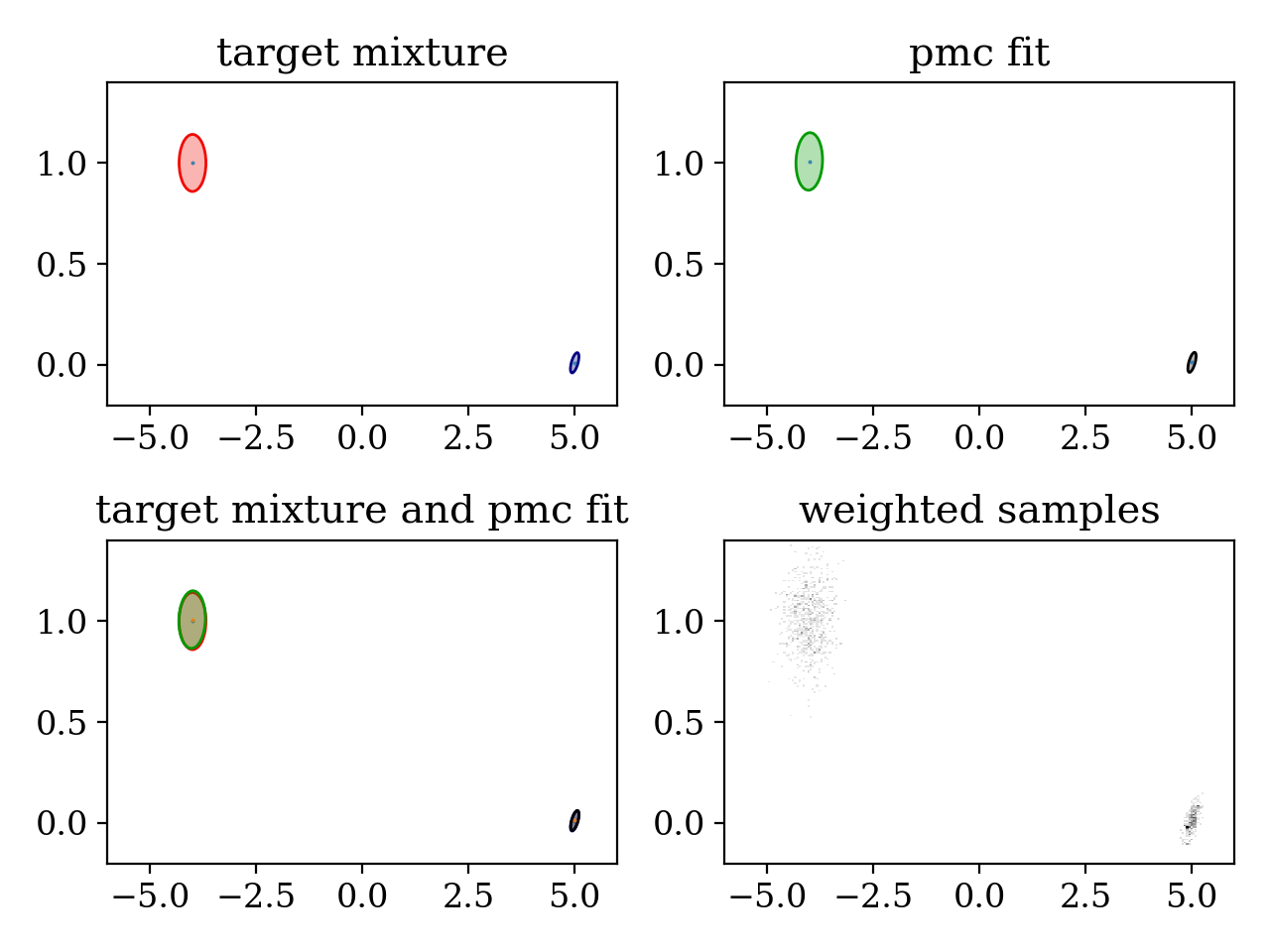

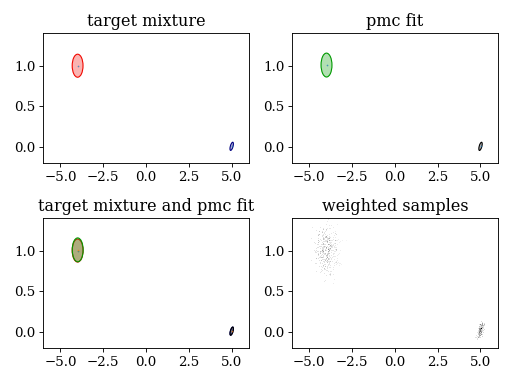

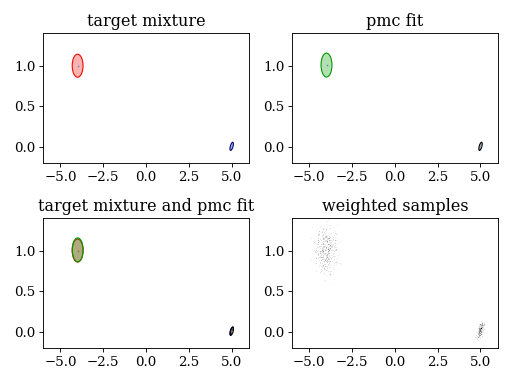

4.2.2. Parallel

'''This example shows how to use importance sampling and how to

adapt the proposal density using the pmc algorithm in an MPI

parallel environment.

In order to have a multiprocessing enviroment invoke this script with

"mpirun -n 10 python pmc_mpi.py".

'''

from mpi4py.MPI import COMM_WORLD as comm

import numpy as np

import pypmc

import pypmc.tools.parallel_sampler # this submodule is NOT imported by ``import pypmc``

# This script is a parallelized version of the PMC example ``pmc.py``.

# The following lines just define a target density and an initial proposal.

# These steps are exactly the same as in ``pmc.py``:

# define the target; i.e., the function you want to sample from.

# In this case, it is a bimodal Gaussian

#

# Note that the target function "log_target" returns the log of the

# target function.

component_weights = np.array([0.3, 0.7])

mean0 = np.array ([ 5.0 , 0.01 ])

covariance0 = np.array([[ 0.01 , 0.003 ],

[ 0.003, 0.0025]])

inv_covariance0 = np.linalg.inv(covariance0)

mean1 = np.array ([-4.0 , 1.0 ])

covariance1 = np.array([[ 0.1 , 0. ],

[ 0. , 0.02 ]])

inv_covariance1 = np.linalg.inv(covariance1)

component_means = [mean0, mean1]

component_covariances = [covariance0, covariance1]

target_mixture = pypmc.density.mixture.create_gaussian_mixture(component_means, component_covariances, component_weights)

log_target = target_mixture.evaluate

# define the initial proposal density

# In this case it has three Gaussians:

# the initial covariances are set to the unit-matrix,

# the initial component weights are set equal

initial_prop_means = []

initial_prop_means.append( np.array([ 4.0, 0.0]) )

initial_prop_means.append( np.array([-5.0, 0.0]) )

initial_prop_means.append( np.array([ 0.0, 0.0]) )

initial_prop_covariance = np.eye(2)

initial_prop_components = []

for i in range(3):

initial_prop_components.append(pypmc.density.gauss.Gauss(initial_prop_means[i], initial_prop_covariance))

initial_proposal = pypmc.density.mixture.MixtureDensity(initial_prop_components)

# -----------------------------------------------------------------------------------------------------------------------

# In ``pmc.py`` the following line defines the sequential single process sampler:

# sampler = pypmc.sampler.importance_sampling.ImportanceSampler(log_target, initial_proposal)

#

# We now use the parallel MPISampler instead:

SequentialIS = pypmc.sampler.importance_sampling.ImportanceSampler

parallel_sampler = pypmc.tools.parallel_sampler.MPISampler(SequentialIS, target=log_target, proposal=initial_proposal)

# Draw 10,000 samples adapting the proposal every 1,000 samples:

# make sure that every process has a different random number generator seed

if comm.Get_rank() == 0:

seed = np.random.randint(1e5)

else:

seed = None

seed = comm.bcast(seed)

np.random.seed(seed + comm.Get_rank())

generating_components = []

for i in range(10):

# With the invocation "mpirun -n 10 python pmc_mpi.py", there are

# 10 processes which means in order to draw 1,000 samples

# ``parallel_sampler.run(1000//comm.Get_size())`` makes each process draw

# 100 samples.

# Hereby the generating proposal component for each sample in each process

# is returned by ``parallel_sampler.run``.

# In the master process, ``parallel_sampler.run`` is a list containing the

# return values of the sequential ``run`` method of every process.

# In all other processes, ``parallel_sampler.run`` returns the generating

# component for its own samples only.

last_generating_components = parallel_sampler.run(1000//comm.Get_size(), trace_sort=True)

# In addition to the generating components, the ``sampler.run``

# method automatically sends all samples to the master

# process i.e. the process which fulfills comm.Get_rank() == 0.

if comm.Get_rank() == 0:

print("\rstep", i, "...\n\t", end='')

# Now let PMC run only in the master process:

# ``sampler.samples_list`` and ``sampler.weights_list`` store the weighted samples

# sorted by the resposible process:

# The History objects that are held by process i can be accessed via

# ``sampler.<samples/weights>_list[i]``. The master process (i=0) also produces samples.

# Combine the weights and samples to two arrays of 1,000 samples

samples = np.vstack([history_item[-1] for history_item in parallel_sampler.samples_list])

weights = np.vstack([history_item[-1] for history_item in parallel_sampler.weights_list])[:,0]

# The latent variables are stored in ``last_generating_components``.

# ``last_generating_components[i]`` returns an array with the generating

# components of the samples produced by process number "i".

# ``np.hstack(last_generating_components)`` combines the generating components

# from all processes to one array holding all 1,000 entries.

generating_components.append( np.hstack(last_generating_components) )

# adapt the proposal using the samples from all processes

new_proposal = pypmc.mix_adapt.pmc.gaussian_pmc(samples, parallel_sampler.sampler.proposal,

weights, generating_components[-1],

mincount=20, rb=True)

else:

# In order to broadcast the ``new_proposal``, define a dummy variable in the other processes

# see "MPI4Py tutorial", section "Collective Communication": http://mpi4py.scipy.org/docs/usrman/tutorial.html

new_proposal = None

# broadcast the ``new_proposal``

new_proposal = comm.bcast(new_proposal)

# replace the old proposal

parallel_sampler.sampler.proposal = new_proposal

# only the master process shall print out any final information

if comm.Get_rank() == 0:

all_samples = np.vstack([history_item[ :] for history_item in parallel_sampler.samples_list])

all_weights = np.vstack([history_item[ :] for history_item in parallel_sampler.weights_list])

last_samples = np.vstack([history_item[-1] for history_item in parallel_sampler.samples_list])

last_weights = np.vstack([history_item[-1] for history_item in parallel_sampler.weights_list])

print("\rsampling finished", end=', ')

print("collected " + str(len(all_samples)) + " samples")

print( '------------------------------------------')

print('\n')

# print information about the adapted proposal

print('initial component weights:', initial_proposal.weights)

print('final component weights:', parallel_sampler.sampler.proposal.weights)

print('target component weights:', component_weights)

print()

for k, m in enumerate([mean0, mean1, None]):

print('initial mean of component %i:' %k, initial_proposal.components[k].mu)

print('final mean of component %i:' %k, parallel_sampler.sampler.proposal.components[k].mu)

print('target mean of component %i:' %k, m)

print()

print()

for k, c in enumerate([covariance0, covariance1, None]):

print('initial covariance of component %i:\n' %k, initial_proposal.components[k].sigma, sep='')

print()

print('final covariance of component %i:\n' %k, parallel_sampler.sampler.proposal.components[k].sigma, sep='')

print()

print('target covariance of component %i:\n' %k, c, sep='')

print('\n')

if comm.Get_size() == 1:

print('******************************************************')

print('********** NOTE: There is only one process. **********')

print('******** try "mpirun -n 10 python pmc_mpi.py" ********')

print('******************************************************')

# plot results

try:

import matplotlib.pyplot as plt

except ImportError:

print('For plotting "matplotlib" needs to be installed')

exit(1)

def set_axlimits():

plt.xlim(-6.0, +6.000)

plt.ylim(-0.2, +1.401)

plt.subplot(221)

plt.title('target mixture')

pypmc.tools.plot_mixture(target_mixture, cmap='jet')

set_axlimits()

plt.subplot(222)

plt.title('pmc fit')

pypmc.tools.plot_mixture(parallel_sampler.sampler.proposal, cmap='nipy_spectral', cutoff=0.01)

set_axlimits()

plt.subplot(223)

plt.title('target mixture and pmc fit')

pypmc.tools.plot_mixture(target_mixture, cmap='jet')

pypmc.tools.plot_mixture(parallel_sampler.sampler.proposal, cmap='nipy_spectral', cutoff=0.01)

set_axlimits()

plt.subplot(224)

plt.title('weighted samples')

plt.hist2d(last_samples[:,0], last_samples[:,1], weights=last_weights[:,0], cmap='gray_r', bins=200)

set_axlimits()

plt.tight_layout()

plt.show()

(Source code, png, hires.png, pdf)

{kind=link}

{kind=link}

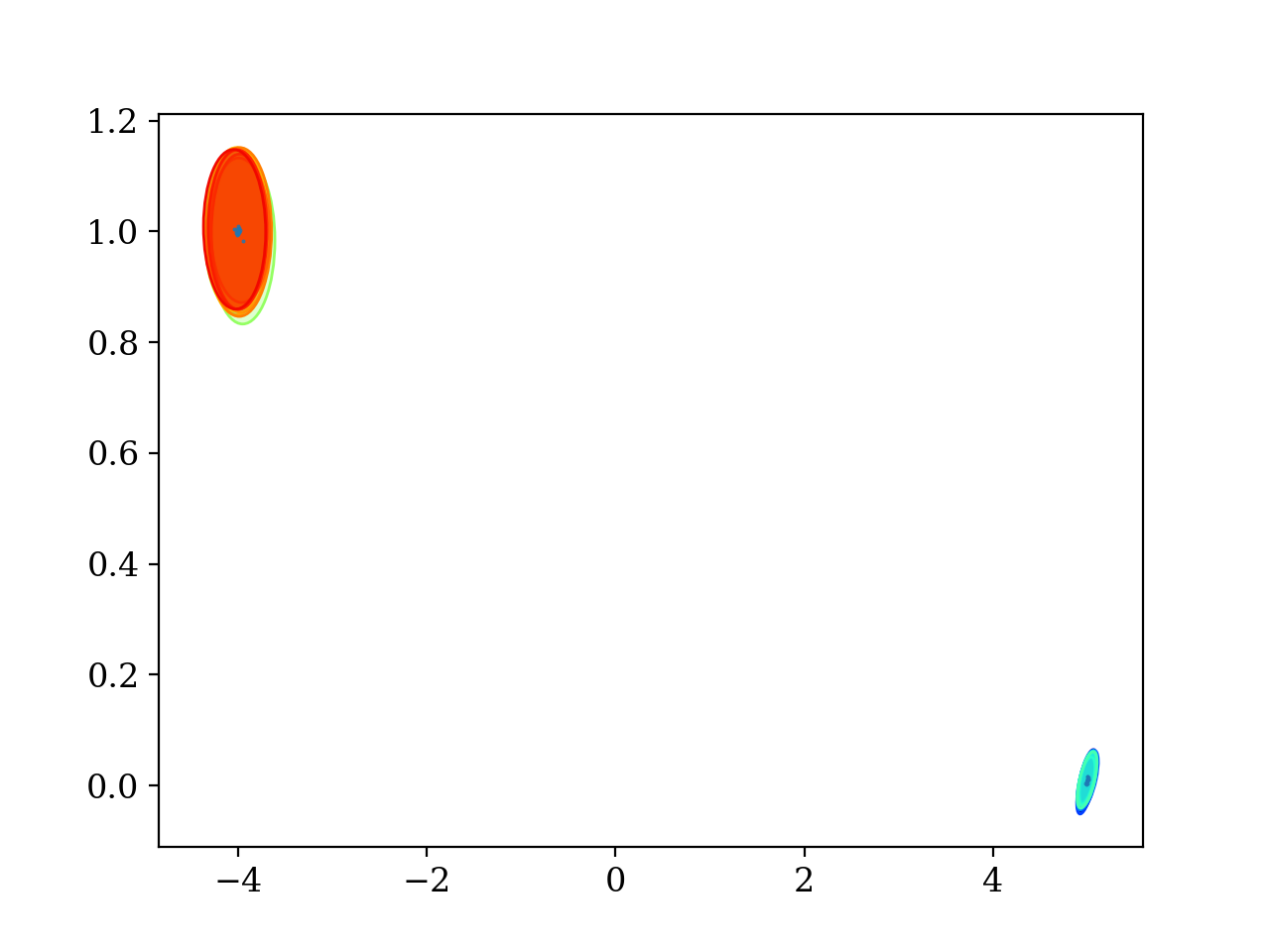

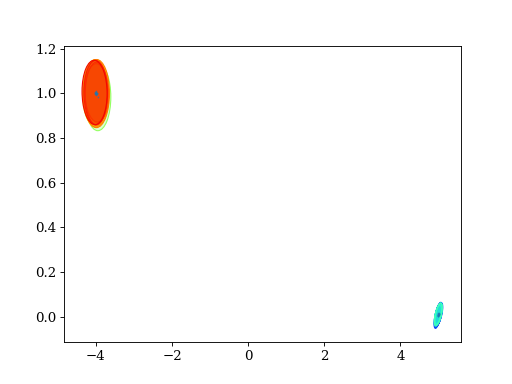

4.3. Grouping by Gelman-Rubin R value

'''This example illustrates how to group Markov Chains according to the

Gelman-Rubin R value (see [GR92]_).

'''

import numpy as np

import pypmc

# A Markov Chain can only explore a local mode of the target function.

# The Gelman-Rubin R value can be used to determine whether N chains

# explored the same mode. Pypmc offers a function which groups chains

# with a common R value less than some ``critical_r``.

#

# In this example, we run five Markov Chains initialized in different

# modes and then group those chains together that explored same mode.

# define a proposal

# this defines the same initial proposal for all chains

prop_dof = 50.

prop_sigma = np.array([[0.1 , 0. ]

,[0. , 0.02]])

prop = pypmc.density.student_t.LocalStudentT(prop_sigma, prop_dof)

# define the target; i.e., the function you want to sample from.

# In this case, it is a bimodal Gaussian with well separated modes.

#

# Note that the target function "log_target" returns the log of the

# target function.

component_weights = np.array([0.3, 0.7])

mean0 = np.array ([ 5.0 , 0.01 ])

covariance0 = np.array([[ 0.01 , 0.003 ],

[ 0.003, 0.0025]])

inv_covariance0 = np.linalg.inv(covariance0)

mean1 = np.array ([-4.0 , 1.0 ])

covariance1 = np.array([[ 0.1 , 0. ],

[ 0. , 0.02 ]])

inv_covariance1 = np.linalg.inv(covariance1)

component_means = [mean0, mean1]

component_covariances = [covariance0, covariance1]

target_mixture = pypmc.density.mixture.create_gaussian_mixture(component_means, component_covariances, component_weights)

log_target = target_mixture.evaluate

# choose initializations for the chains

# Here we place two chains into the mode at [5, 0.01] and three into the mode at [-4,1].

# In such a setup, the chains will only explore the mode where they are initialized.

# Different random numbers are used in each chain.

starts = [np.array([4.999, 0.])] * 2 + [np.array([-4.0001, 0.999])] * 3

# define the markov chain objects

mcs = [pypmc.sampler.markov_chain.AdaptiveMarkovChain(log_target, prop, start) for start in starts]

# run and discard burn-in

for mc in mcs:

mc.run(10**2)

mc.clear()

# run 10,000 steps adapting the proposal every 500 steps

for mc in mcs:

for i in range(20):

mc.run(500)

mc.adapt()

# extract a reference to the samples from all chains

stacked_values = [mc.samples[:] for mc in mcs]

# find the chain groups

# chains 0 and 1 are initialized in the same mode (at [5, 0.01])

# chains 2, 3 and 4 are initialized in the same mode (at [-4, 0])

# expect chain groups:

expected_groups = [[0,1], [2,3,4]]

# R value calculation only needs the means, variances (diagonal

# elements of covariance matrix) and number of samples,

# axis=0 ensures that we get variances separately for each parameter.

# critical_r can be set manually, here the default value is used

found_groups = pypmc.mix_adapt.r_value.r_group([np.mean(chain, axis=0) for chain in stacked_values],

[np.var (chain, axis=0) for chain in stacked_values],

len(stacked_values[0]))

# print the result

print("Expect %s" % expected_groups)

print("Have %s" % found_groups)

# Hint: ``stacked_values`` is an example of what `pypmc.mix_adapt.r_value.make_r_gaussmix()` expects as ``data``

result = pypmc.mix_adapt.r_value.make_r_gaussmix(stacked_values)

try:

import matplotlib.pyplot as plt

except ImportError:

print('For plotting "matplotlib" needs to be installed')

exit(1)

pypmc.tools.plot_mixture(result, cmap='jet')

plt.show()

(Source code, png, hires.png, pdf)

{kind=link}

{kind=link}

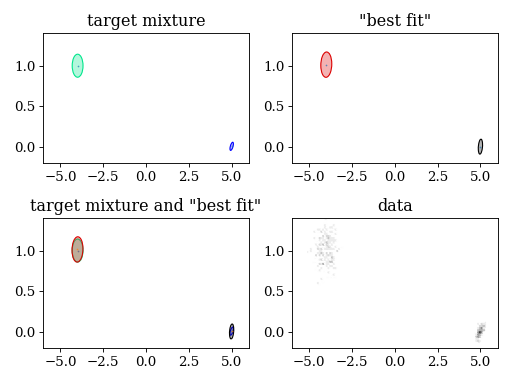

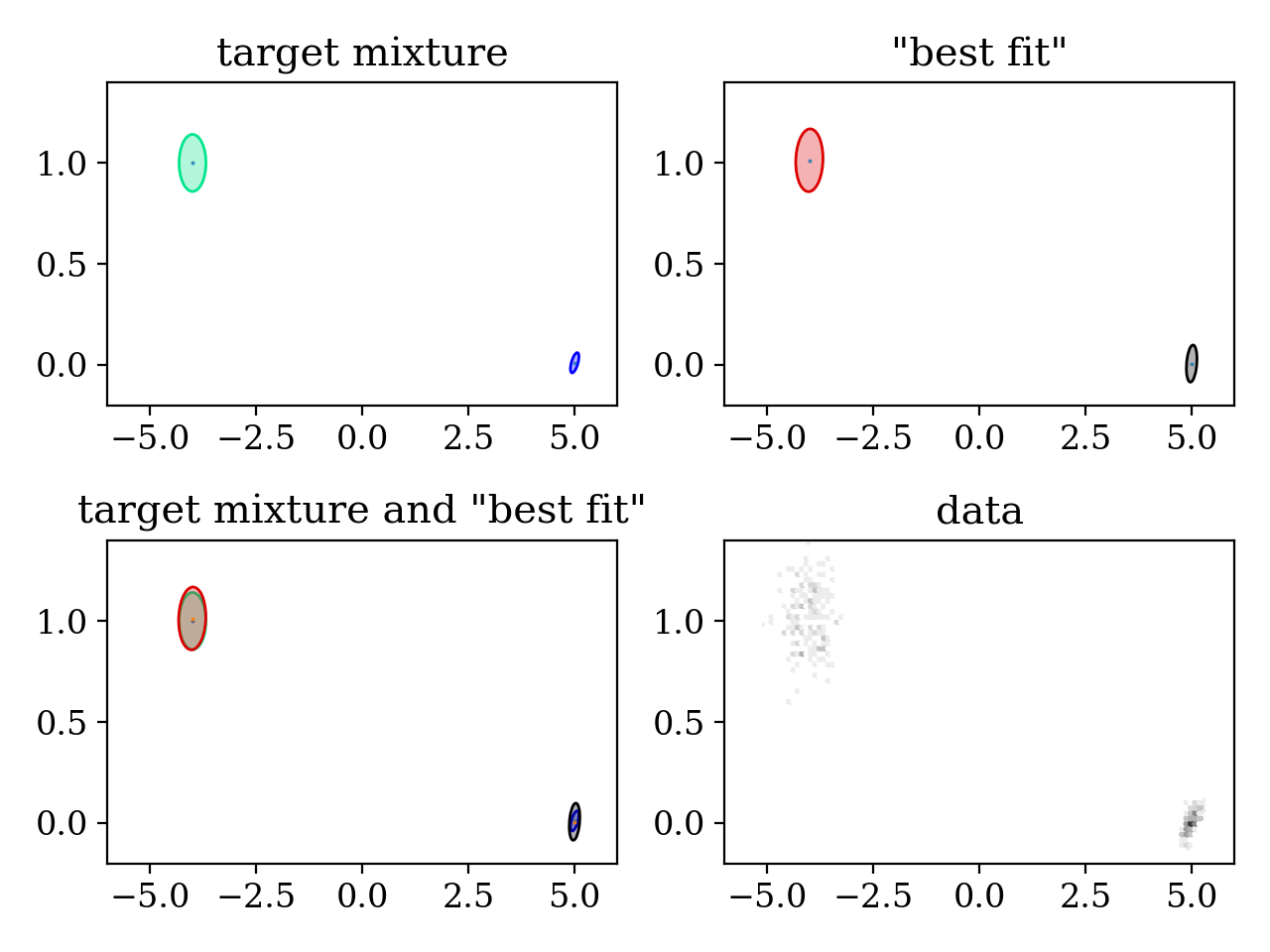

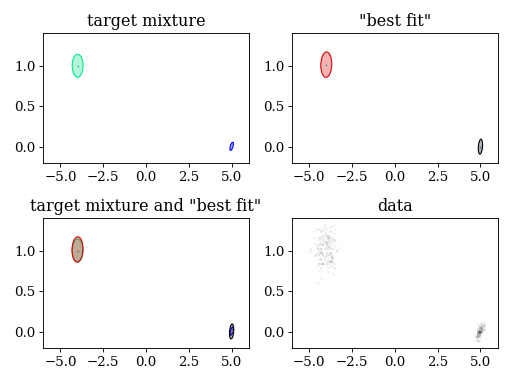

4.4. Variational Bayes

'''This example shows how to generate a "best fit" Gaussian mixture density

from data using variational Bayes.

'''

## in this example, we will:

## 1. Define a Gaussian mixture

## 2. Generate demo data from that Gaussian mixture

## 3. Generate a Gaussian mixture out of the data

## 4. Plot the original and the generated mixture

import numpy as np

import pypmc

# -------------------- 1. Define a Gaussian mixture --------------------

component_weights = np.array([0.3, 0.7])

mean0 = np.array ([ 5.0 , 0.01 ])

covariance0 = np.array([[ 0.01 , 0.003 ],

[ 0.003, 0.0025]])

mean1 = np.array ([-4.0 , 1.0 ])

covariance1 = np.array([[ 0.1 , 0. ],

[ 0. , 0.02 ]])

component_means = [mean0, mean1]

component_covariances = [covariance0, covariance1]

target_mix = pypmc.density.mixture.create_gaussian_mixture(component_means, component_covariances, component_weights)

# -------------------- 2. Generate demo data ---------------------------

data = target_mix.propose(500)

# -------------------- 3. Adapt a Gaussian mixture ---------------------

# maximum number of components

K = 20

# Create a "GaussianInference" object.

# The following command passes just the two essential arguments to "GaussianInference":

# The ``data`` and a maximum number of ``components``.

# For reasonable results in more complicated settings, a careful choice for ``W0``

# is crucial. As a rule of thumb, choose ``inv(W0)`` much smaller than the expected

# covariance. In this case, however, the default (``W0`` = unit matrix) is good enough.

vb = pypmc.mix_adapt.variational.GaussianInference(data, K)

# adapt the variational parameters

converged = vb.run(100, verbose=True)

print('-----------------------------')

# generate a Gaussian mixture with the most probable parameters

fit_mixture = vb.make_mixture()

# -------------------- 4. Plot/print results ---------------------------

if converged is None:

print('\nThe adaptation did not converge.\n')

else:

print('\nConverged after %i iterations.\n' %converged)

print("final component weights: " + str(fit_mixture.weights))

print("target component weights: " + str( target_mix.weights))

try:

import matplotlib.pyplot as plt

except ImportError:

print('For plotting "matplotlib" needs to be installed')

exit(1)

def set_axlimits():

plt.xlim(-6.0, +6.000)

plt.ylim(-0.2, +1.401)

plt.subplot(221)

plt.title('target mixture')

pypmc.tools.plot_mixture(target_mix, cmap='winter')

set_axlimits()

plt.subplot(222)

plt.title('"best fit"')

pypmc.tools.plot_mixture(fit_mixture, cmap='nipy_spectral')

set_axlimits()

plt.subplot(223)

plt.title('target mixture and "best fit"')

pypmc.tools.plot_mixture(target_mix, cmap='winter')

pypmc.tools.plot_mixture(fit_mixture, cmap='nipy_spectral')

set_axlimits()

plt.subplot(224)

plt.title('data')

plt.hexbin(data[:,0], data[:,1], cmap='gray_r')

set_axlimits()

plt.tight_layout()

plt.show()

(Source code, png, hires.png, pdf)

{kind=link}

{kind=link}

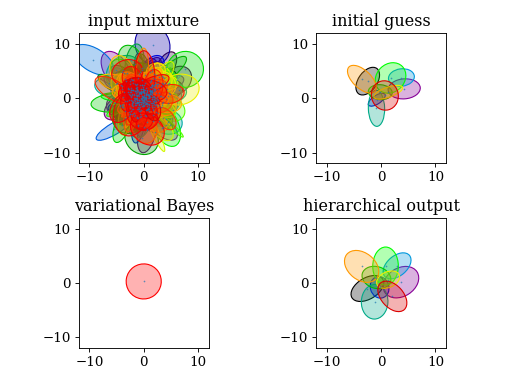

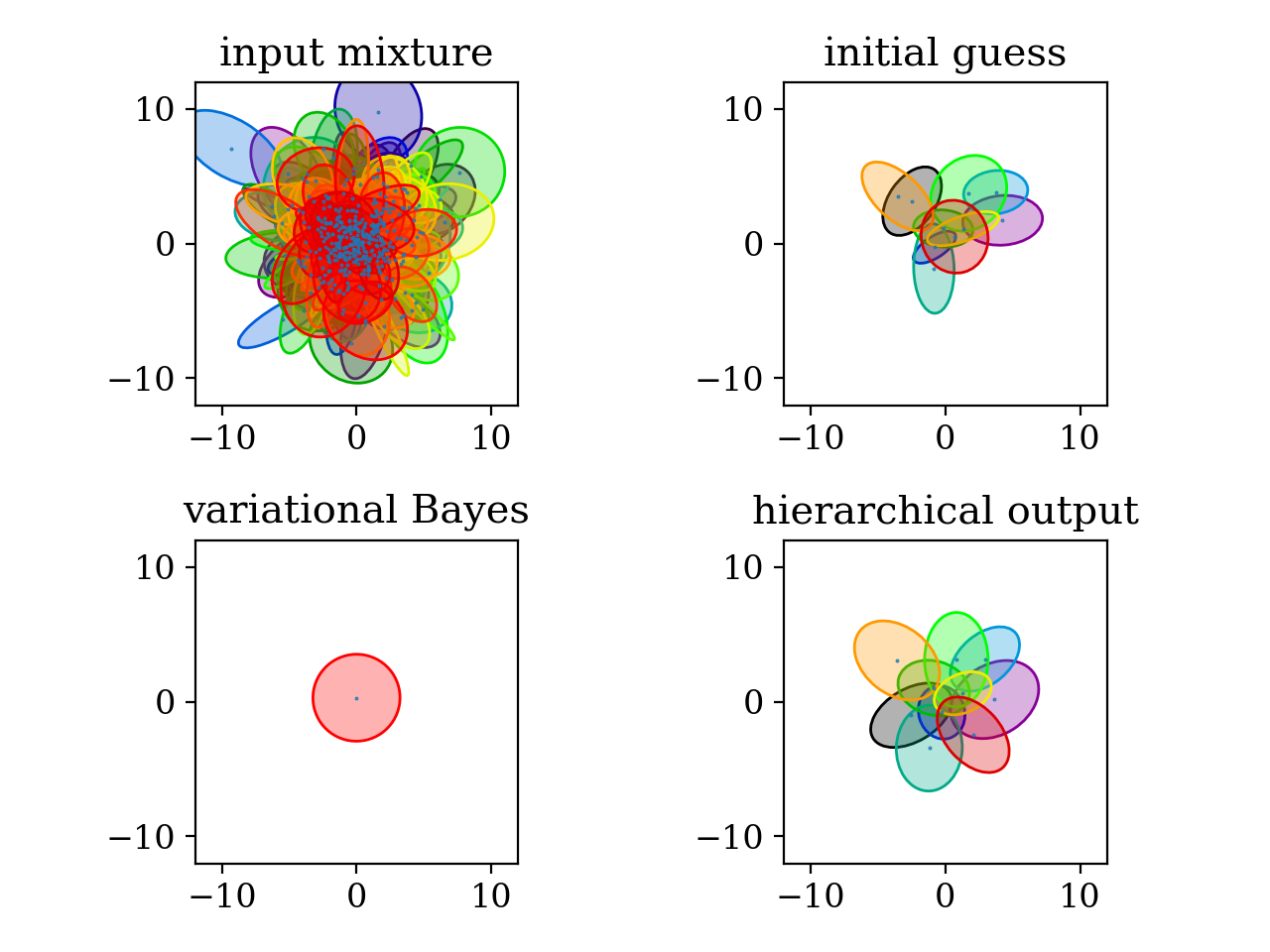

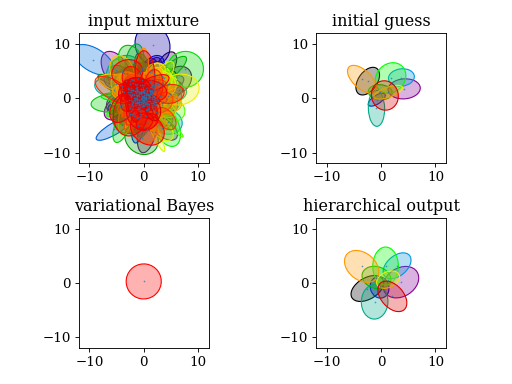

4.5. Mixture reduction

'''Demonstrate the usage of hierarchical clustering and variational

Bayes (VBMerge) to reduce a given Gaussian mixture to a Gaussian

mixture with a reduced number of components.

'''

import numpy as np

from scipy.stats import chi2

import pypmc

# dimension

D = 2

# number of components

K = 400

# Wishart parameters: mean W, degree of freedom nu

W = np.eye(D)

nu = 5

# "draw" covariance matrices from Wishart distribution

def wishart(nu, W):

dim = W.shape[0]

chol = np.linalg.cholesky(W)

tmp = np.zeros((dim,dim))

for i in range(dim):

for j in range(i+1):

if i == j:

tmp[i,j] = np.sqrt(chi2.rvs(nu-(i+1)+1))

else:

tmp[i,j] = np.random.normal(0,1)

return np.dot(chol, np.dot(tmp, np.dot(tmp.T, chol.T)))

covariances = [wishart(nu, W) for k in range(K)]

# put components at positions drawn from a Gaussian around mu

mu = np.zeros(D)

means = [np.random.multivariate_normal(mu, sigma) for sigma in covariances]

# equal weights for every component

weights = np.ones(K)

# weights are automatically normalized

input_mixture = pypmc.density.mixture.create_gaussian_mixture(means, covariances, weights)

# create initial guess from first K_out components

K_out = 10

initial_guess = pypmc.density.mixture.create_gaussian_mixture(means[:K_out], covariances[:K_out], weights[:K_out])

###

# hierarchical clustering

#

# - the output closely resembles the initial guess

# - components laid out spherically symmetric

# - every component is preserved

###

h = pypmc.mix_adapt.hierarchical.Hierarchical(input_mixture, initial_guess)

h.run(verbose=True)

###

# VBMerge

#

# - N is the number of samples that gave rise to the input mixture. It

# is arbitrary, so play around with it. You might have to adjust the

# ``prune`` parameter in the ``run()`` method

# - only one component survives, again it is spherically symmetric

###

vb = pypmc.mix_adapt.variational.VBMerge(input_mixture, N=1000,

initial_guess=initial_guess)

print()

print("Start variational Bayes:")

vb.run(verbose=True)

# plot results

try:

import matplotlib.pyplot as plt

except ImportError:

print('For plotting "matplotlib" needs to be installed')

exit(1)

def set_axlimits():

plt.gca().set_aspect('equal')

plt.xlim(-12.0, +12.0)

plt.ylim(-12.0, +12.0)

plt.subplot(221)

plt.title('input mixture')

pypmc.tools.plot_mixture(input_mixture)

set_axlimits()

plt.subplot(222)

plt.title('initial guess')

pypmc.tools.plot_mixture(initial_guess)

set_axlimits()

plt.subplot(223)

plt.title('variational Bayes')

pypmc.tools.plot_mixture(vb.make_mixture(), cmap='autumn')

set_axlimits()

plt.subplot(224)

plt.title('hierarchical output')

pypmc.tools.plot_mixture(h.g)

set_axlimits()

plt.tight_layout()

plt.show()

(Source code, png, hires.png, pdf)

{kind=link}

{kind=link}

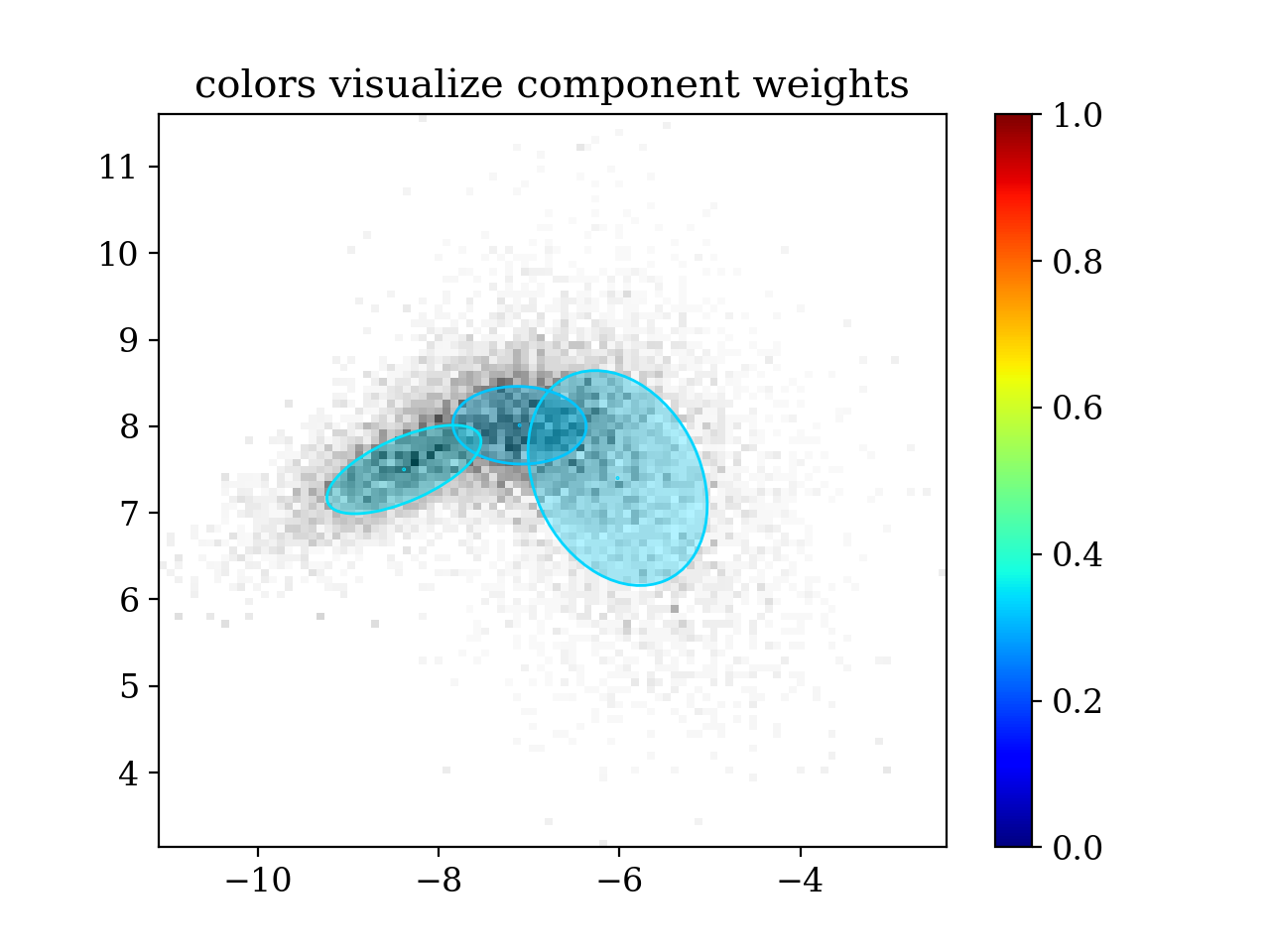

4.6. MCMC + variational Bayes

'''This example illustrates how pypmc can be used to integrate a

non-negative function. The presented algorithm needs very little

analytical knowledge about the function.

'''

import numpy as np

import pypmc

# The idea is to find a good proposal function for importance sampling

# with as little information about the target function as possible.

#

# In this example we will first map out regions of interest using Markov

# chains, then we use the variational Bayes to approximate the target

# with a Gaussian mixture.

# *************************** Important: ***************************

# * The target function must be defined such that it returns the *

# * log of the function of interest. The methods we use imply that *

# * the function is interpreted as an unnormalized probability *

# * density. *

# ******************************************************************

# Define the target; i.e., the function you want to sample from. In

# this case, it is a Student's t mixture of three components with

# different degrees of freedom. They are located close to each other.

# If you want a multimodal target, adjust the means.

dim = 2

mean0 = np.array ([-6.0, 7.3 ])

covariance0 = np.array([[ 0.8, -0.3 ],

[-0.3, 1.25]])

mean1 = np.array ([-7.0, 8.0 ])

covariance1 = np.array([[ 0.5, 0. ],

[ 0. , 0.2 ]])

mean2 = np.array ([-8.5, 7.5 ])

covariance2 = np.array([[ 0.5, 0.2 ],

[ 0.2, 0.2 ]])

component_weights = np.array([0.3, 0.4, 0.3])

component_means = [mean0, mean1, mean2]

component_covariances = [covariance0, covariance1, covariance2]

dofs = [13, 17, 5]

target_mixture = pypmc.density.mixture.create_t_mixture(component_means, component_covariances, dofs, component_weights)

log_target = target_mixture.evaluate

# Now we suppose that we only have the following knowledge about the

# target function: its regions of interest are at a distance of no more

# than order ten from zero.

# Now we try to find these with Markov chains. We have to deal with

# the fact that there may be modes separated by regions of very low

# probability. It is thus unlikely that a single chain explores more

# than one mode in such a case. To deal with this multimodality, we

# start several chains and hope that they find all modes. We will

# start ten Markov chains at random positions in the square

# [(-10,-10), (+10,+10)].

starts = [np.random.uniform(-10,10, size=dim) for i in range(10)]

# For a local-random-walk Markov chain, we also need an initial

# proposal. Here, we take a gaussian with initial covariance

# diag(1e-3). The initial covariance should be chosen such that it is

# of the same order as the real covariance of the mode to be mapped

# out. For a Gaussian target, the overall scale should

# decrease as 2.38^2/d as the dimension d increases to achieve an

# acceptance rate around 20%.

mc_prop = pypmc.density.gauss.LocalGauss(np.eye(dim) * 2.38**2 / dim)

mcs = [pypmc.sampler.markov_chain.AdaptiveMarkovChain(log_target, mc_prop, start) for start in starts]

print('running Markov chains ...')

# In general we need to let the chain move to regions of high

# probability, these samples are not representative, so we discard them

# as burn-in. Then we let the Markov chains map out the regions of

# interest. The samples are used to adapt the proposal covariance to

# yield a satisfactory acceptance rate.

for mc in mcs:

for i in range(20):

mc.run(500)

mc.adapt()

if i == 0:

mc.clear()

mc_samples_sorted_by_chain = [mc.samples[:] for mc in mcs]

mc_samples = np.vstack(mc_samples_sorted_by_chain)

means = np.zeros((len(mcs), dim))

variances = np.zeros_like(means)

for i,mc in enumerate(mc_samples_sorted_by_chain):

means[i] = mc.mean(axis=0)

variances[i] = mc.var(axis=0)

# Now we use the Markov chain samples to generate a mixture proposal

# function for importance sampling. For this purpose, we choose the

# variational Bayes algorithm that takes samples and an initial guess

# of the mixture as input. To create the initial guess, we group all

# chains that mixed, and create 10 components per group. For a

# unimodal target, all chains should mix. For more information about

# the following call, check the example "Grouping by Gelman-Rubin R

# value"(r-group.py) or the reference documentation.

long_patches = pypmc.mix_adapt.r_value.make_r_gaussmix(mc_samples_sorted_by_chain, K_g=10)

# Comments on arguments:

# o mc_samples[::100] - Samples in the Markov chains are strongly correlated

# => thin the samples to get approx. independent samples

# o W0=np.eye(dim)*1e10 - The resulting covariance matrices can be very

# sensitive to W0. Its inverse should be chosen much

# smaller than the actual covariance. If it is too small,

# W0 will dominate the resulting covariances and

# usually lead to very bad results.

vb = pypmc.mix_adapt.variational.GaussianInference(mc_samples[::100], initial_guess=long_patches, W0=np.eye(dim)*1e10)

# When we run variational Bayes, we want unneccessary components to be

# automatically pruned. The prune parameter sets how many samples a

# component must effectively have to be considered important. The rule

# of thumb employed here proved good in our experiments.

vb_prune = 0.5 * len(vb.data) / vb.K

# Run the variational Bayes for at most 1,000 iterations. But if the

# lower bound of the model evidence changes by less than `rel_tol`,

# convergence is declared before. If we increase `rel_tol` to 1e-4, it

# takes less iterations but potentially more (useless) components

# survive the pruning. The trade-off depends on the complexity of the

# problem.

print('running variational Bayes ...')

vb.run(1000, rel_tol=1e-8, abs_tol=1e-5, prune=vb_prune, verbose=True)

# extract the most probable Gaussian mixture given the samples

vbmix = vb.make_mixture()

# Now we can instantiate an importance sampler. We draw 1,000

# importance samples and use these for a proposal update using

# variational Bayes again. In case there are multiple modes and

# the chains did not mix, we need this step to infer the right

# component weights because the component weight is given by

# how many chains it attracted, which could be highly dependent

# on the starting points and independent of the correct

# probability mass.

print('running importance sampling ...')

sampler = pypmc.sampler.importance_sampling.ImportanceSampler(log_target, vbmix)

sampler.run(1000)

# The variational Bayes allows us, unlike PMC, to include the

# information gained by the Markov chains in subsequent proposal

# updates. We know that we cannot trust the component weights obtained

# by the chains. Nevertheless, we can rely on the means and covariances. The

# following lines show how to code that into the variational Bayes by

# removing the hyperparameter `alpha0` that encodes the component

# weights.

prior_for_proposal_update = vb.posterior2prior()

prior_for_proposal_update.pop('alpha0')

vb2 = pypmc.mix_adapt.variational.GaussianInference(sampler.samples[:],

initial_guess=vbmix,

weights=sampler.weights[:][:,0],

**prior_for_proposal_update)

# Note: This time we leave "prune" at the default value "1" because we

# want to keep all components that are expected to contribute

# with at least one effective sample per importance sampling run.

print('running variational Bayes ...')

vb2.run(1000, rel_tol=1e-8, abs_tol=1e-5, verbose=True)

vb2mix = vb2.make_mixture()

# Now we draw another 10,000 samples with the updated proposal

sampler.proposal = vb2mix

print('running importance sampling ...')

sampler.run(10**4)

# We can combine the samples and weights from the two runs, see reference [Cor+12].

weights = pypmc.sampler.importance_sampling.combine_weights([samples[:] for samples in sampler.samples],

[weights[:][:,0] for weights in sampler.weights],

[vbmix, vb2mix] ) \

[:][:,0]

samples = sampler.samples[:]

# The integral can then be estimated from the weights. The error is also

# estimated from the weights. By the central limit theorem, the integral

# estimator has a gaussian distribution.

integral_estimator = weights.sum() / len(weights)

integral_uncertainty_estimator = np.sqrt((weights**2).sum() / len(weights) - integral_estimator**2) / np.sqrt(len(weights)-1)

print('analytical integral = 1')

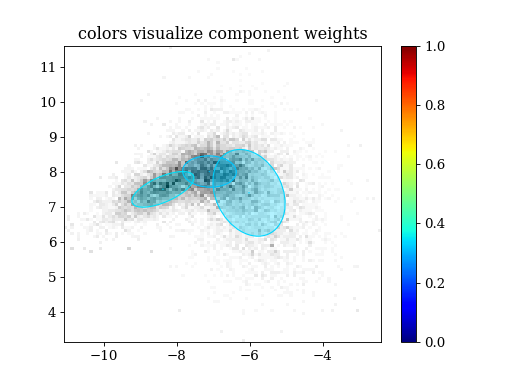

print('estimated integral =', integral_estimator, '+-', integral_uncertainty_estimator)

# Let's see how good the proposal matches the target density: the closer

# the values of perplexity and effective sample size (ESS) are to 1,

# the better. Outliers, or samples out in the tails of the target

# with a very large weight, show up in the 2D marginal and reduce the

# ESS significantly. For the above integral estimate to be right on

# average, they are 'needed'. Without outliers (most of the time), the

# integral is a tad too small.

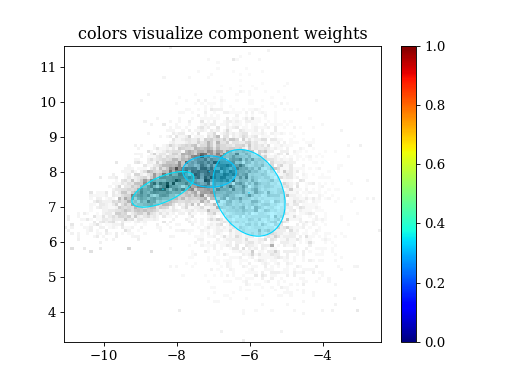

print('perplexity', pypmc.tools.convergence.perp(weights))

print('effective sample size', pypmc.tools.convergence.ess(weights))

# As mentioned in the very beginning, the methods we applied reinterpret

# the target function as an unnormalized probability density.

# In addition to the integral, we also get weighted samples distributed according

# to that probability density.

try:

import matplotlib.pyplot as plt

except ImportError:

print('For plotting "matplotlib" needs to be installed')

exit(1)

plt.figure()

plt.hist2d(samples[:,0], samples[:,1], weights=weights, bins=100, cmap='gray_r')

pypmc.tools.plot_mixture(sampler.proposal, visualize_weights=True, cmap='jet')

plt.colorbar()

plt.clim(0.0, 1.0)

plt.title('colors visualize component weights')

plt.show()

(Source code, png, hires.png, pdf)

{kind=link}

{kind=link}